Deep Learning with Softmax and SVM using Worst Omega Optimization for Multi-Class Financial Prediction

DOI:

https://doi.org/10.58190/imiens.2026.169Keywords:

Deep Learning, Classification, Support Vector Machine, Optimization, Data analysis and predictionAbstract

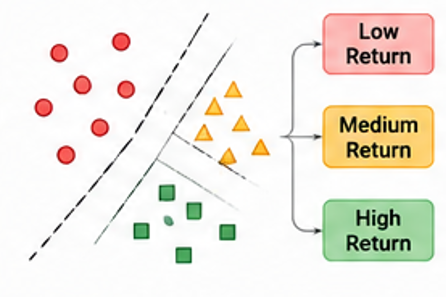

This study proposes a hybrid framework for multi-class financial prediction and portfolio optimization by integrating deep learning-based classification models with worst-case Omega optimization. The framework employs a neural network architecture combined with Softmax and multi-class Support Vector Machine (SVM) classifiers to categorize assets into low-, medium-, and high-return classes. These classifications are subsequently utilized to construct portfolios using a worst-case Omega optimization model that explicitly accounts for downside risk and uncertainty. The empirical analysis is conducted on two benchmark datasets, BSE 30 and DOW 30, using a rolling window approach. The results demonstrate that the SVM-based classification model outperforms the Softmax model in terms of class separability and stability across varying market conditions. Portfolios constructed using SVM-selected assets consistently achieve higher returns, lower volatility, and improved risk-adjusted performance, as evidenced by superior Sharpe, Sortino, STARR, and Omega ratios. Furthermore, the worst-case Omega optimization framework provides enhanced protection against extreme losses by effectively controlling tail risk, as reflected in lower Value-at-Risk (VaR) and Conditional Value-at-Risk (CVaR). Comparative analysis with equally weighted portfolios confirms the ability of the proposed framework to generate persistent excess returns across different risk-aversion levels. Overall, the study highlights the importance of combining accurate classification techniques with robust optimization methods for effective portfolio management. The proposed approach offers a flexible and reliable solution for decision-making in dynamic and uncertain financial markets.

Downloads

References

H. Markowitz, “Modern portfolio theory,” J. Finance, vol. 7, no. 11, pp. 77–91, 1952.

[2] H. Markowitz, “The utility of wealth,” J. Polit. Econ., vol. 60, no. 2, pp. 151–158, 1952.

[3] Y. LeCun, Y. Bengio, and G. Hinton, “Deep learning,” nature, vol. 521, no. 7553, pp. 436–444, 2015.

[4] T. Fischer and C. Krauss, “Deep learning with long short-term memory networks for financial market predictions,” Eur. J. Oper. Res., vol. 270, no. 2, pp. 654–669, 2018.

[5] J. B. Heaton, N. G. Polson, and J. H. Witte, “Deep learning for finance: deep portfolios,” Appl. Stoch. Models Bus. Ind., vol. 33, no. 1, pp. 3–12, 2017.

[6] M. Ashrafzadeh, M. Sadrani, and S. H. Zolfani, “Deep learning and machine learning models for portfolio optimization: Enhancing return prediction with stock clustering,” Results Eng., p. 106263, 2025.

[7] Y. Zhang, Y. Liu, W. Liu, and X. Yang, “An end-to-end deep learning framework for the portfolio optimization with stop-loss orders,” Appl. Soft Comput., vol. 181, p. 113465, 2025.

[8] W. Huang, Y. Nakamori, and S.-Y. Wang, “Forecasting stock market movement direction with support vector machine,” Comput. Oper. Res., vol. 32, no. 10, pp. 2513–2522, 2005.

[9] C. Cortes and V. Vapnik, “Support-vector networks,” Mach. Learn., vol. 20, no. 3, pp. 273–297, 1995.

[10] S. Gu, B. Kelly, and D. Xiu, “Empirical asset pricing via machine learning,” Rev. Financ. Stud., vol. 33, no. 5, pp. 2223–2273, 2020.

[11] X. Martínez-Barbero, R. Cervelló-Royo, and J. Ribal, “Portfolio optimization with prediction-based return using long short-Term memory neural networks: testing on upward and downward European markets,” Comput. Econ., vol. 65, no. 3, pp. 1479–1504, 2025.

[12] C. Keating and W. F. Shadwick, “A universal performance measure,” J. Perform. Meas., vol. 6, no. 3, pp. 59–84, 2002.

[13] N. Tewari, M. I. H. Showrov, and V. K. Dubey, “A Review of Omega Based Portfolio Optimization,” in 2019 International Conference on Power Electronics, Control and Automation (ICPECA), IEEE, 2019, pp. 1–5.

[14] M. Kapsos, S. Zymler, N. Christofides, and B. Rustem, “Optimizing the Omega ratio using linear programming,” J. Comput. Finance, vol. 17, no. 4, pp. 49–57, 2014.

[15] S. Kaur, A. Singh, and A. Aggarwal, “Mean-Variance optimal portfolio selection integrated with support vector and fuzzy support vector machines,” J. Fuzzy Ext. Appl., vol. 5, no. 3, pp. 434–468, 2024, doi: 10.22105/jfea.2024.453926.1453.

[16] S. Kaur, “From Sentiment to Strategy: Machine Learning in Emotion-Based Asset Allocation,” IntechOpen, 2025.

[17] S. Kaur, A. Singh, and A. Aggarwal, “Optimal portfolio construction with fuzzy least square support vector machines and conditional value-at-risk: a risk-adjusted approach,” Int. J. Syst. Assur. Eng. Manag., pp. 1–35, 2025.

[18] S. Kaur, A. Singh, and A. Aggarwal, “A Novel Fuzzy Multi-Class Support Vector Machine: An Application to Asset Selection and Portfolio Optimization,” Comput. Econ., pp. 1–46, 2025.

[19] R. Yan, J. Jin, and K. Han, “Reinforcement learning for deep portfolio optimization,” Electron. Res. Arch., vol. 32, no. 9, pp. 5176–5200, 2024, doi: 10.3934/era.2024239.

[20] H. Choudhary, A. Orra, K. Sahoo, and M. Thakur, “Risk-Adjusted Deep Reinforcement Learning for Portfolio Optimization: A Multi-reward Approach,” Int. J. Comput. Intell. Syst., vol. 18, p. 126, 2025, doi: 10.1007/s44196-025-00875-8.

[21] F. Gu, Z. Jiang, A. F. Garcia-Fernandez, A. Stefanidis, J. Su, and H. Li, “MTS: A Deep Reinforcement Learning Portfolio Management Framework with Time-Awareness and Short-Selling,” ArXiv Prepr. ArXiv250304143, 2025.

[22] A. Charkhestani and A. Esfahanipour, “Behaviorally informed deep reinforcement learning for portfolio optimization with loss aversion and overconfidence,” Sci. Rep., vol. 16, p. 6443, 2026, doi: 10.1038/s41598-026-35902-x.

[23] F. J. Fabozzi, P. N. Kolm, D. A. Pachamanova, and S. M. Focardi, Robust portfolio optimization and management. John Wiley & Sons, 2007.

[24] L. Kevin et al., “Hybrid Deep Learning for Detecting Hate Speech Across Social Media Platforms,” in Current and Future Trends on AI Applications: Volume 1, Springer, 2025, pp. 289–304.

[25] A. Ben-Tal, D. Den Hertog, A. De Waegenaere, B. Melenberg, and G. Rennen, “Robust solutions of optimization problems affected by uncertain probabilities,” Manag. Sci., vol. 59, no. 2, pp. 341–357, 2013.

[26] X. Ren, N. Abudurexiti, Z. Jiang, A. Stefanidis, H. Liu, and J. Su, “SAMP-HDRL: Segmented Allocation with Momentum-Adjusted Utility for Multi-agent Portfolio Management via Hierarchical Deep Reinforcement Learning,” ArXiv Prepr. ArXiv251222895, 2025.

[27] N. Ranabhat, B. Javanparast, D. Goerz, and E. Inack, “Large-scale portfolio optimization with variational neural annealing,” ArXiv Prepr. ArXiv250707159, 2025.

[28] Y. Tang, “Deep learning using support vector machines,” CoRR Abs13060239, vol. 2, no. 1, 2013.

[29] Y. Ma, W. Wang, and Q. Ma, “A novel prediction based portfolio optimization model using deep learning,” Comput. Ind. Eng., vol. 177, p. 109023, 2023.

Downloads

Published

Issue

Section

License

Copyright (c) 2026 Intelligent Methods In Engineering Sciences

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.

How to Cite